A GCR special report into the surge of power construction that will transform the continent over the next six years.

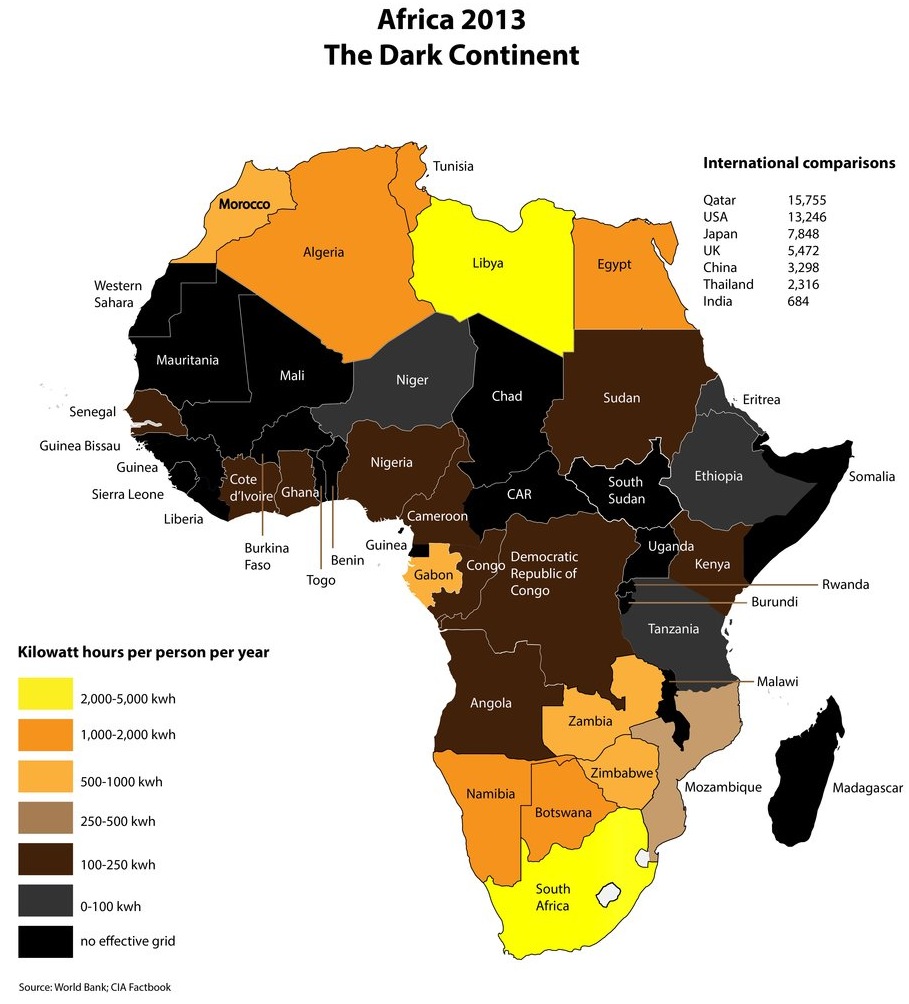

Sub-Saharan Africa is made up of 49 countries, with a total population of about 826 million. Together, they have an installed generating capacity of 68GW. This is equivalent to the electricity output of Iran (62GW). About 65% of this capacity is provided by one country: South Africa.

The main actor in the transformation of Africa has been Chinese capital, more recently joined by India and, in the Maghreb, the Gulf states–

Unfortunately, the generating equipment, substations and grids of these 49 countries are often in need of repair or replacement, which means that available power is well below installed capacity: in countries that have suffered civil war, such as the Democratic Republic of Congo (DRC), only 48% of installed capacity finds its way to a plug socket. Â

The result of all this is in about 80% of Sub-Saharan Africa, cooking is accomplished by burning wood or other biomass and lighting is by means of oil lamps. What electricity there is is produced by expensive diesel generators.

The present situation is the result of a century of under-investment. The World Bank estimates that external spending on the entire continent’s power sector has been $600m a year – hardly enough to maintain what is there now. It is clear that a surge in investment is needed to refurbish the existing infrastructure and create national and international grids before they will be able to distribute additional generating capacity. Â

This is now changing. The main actor in the transformation of Africa has been Chinese capital, more recently joined by India and, in the Maghreb, the Gulf states. The financing is funding the exploitation of the continent’s vast reserves of fossil fuel, and its potential reserves of renewables and hydroelectric power.

This extra power will then allow the exploitation of mineral resources, and so make available more money for the power sector. This virtuous circle may eventually make possible a wider transformation of ordinary life, such as allowing schoolchildren sufficient light to do homework, or allowing municipal governments to think about commissioning public transport systems.Â

In some cases, such as Ethiopia and the DRC, the country’s entire future has been predicated on electricity generation. The former’s Grand Renaissance Dam is being partly financed by bonds bought by the population; the latter’s Great Inga Dam may eventually provide two-thirds of the whole of Sub-Saharan Africa’s present generating capacity.Â

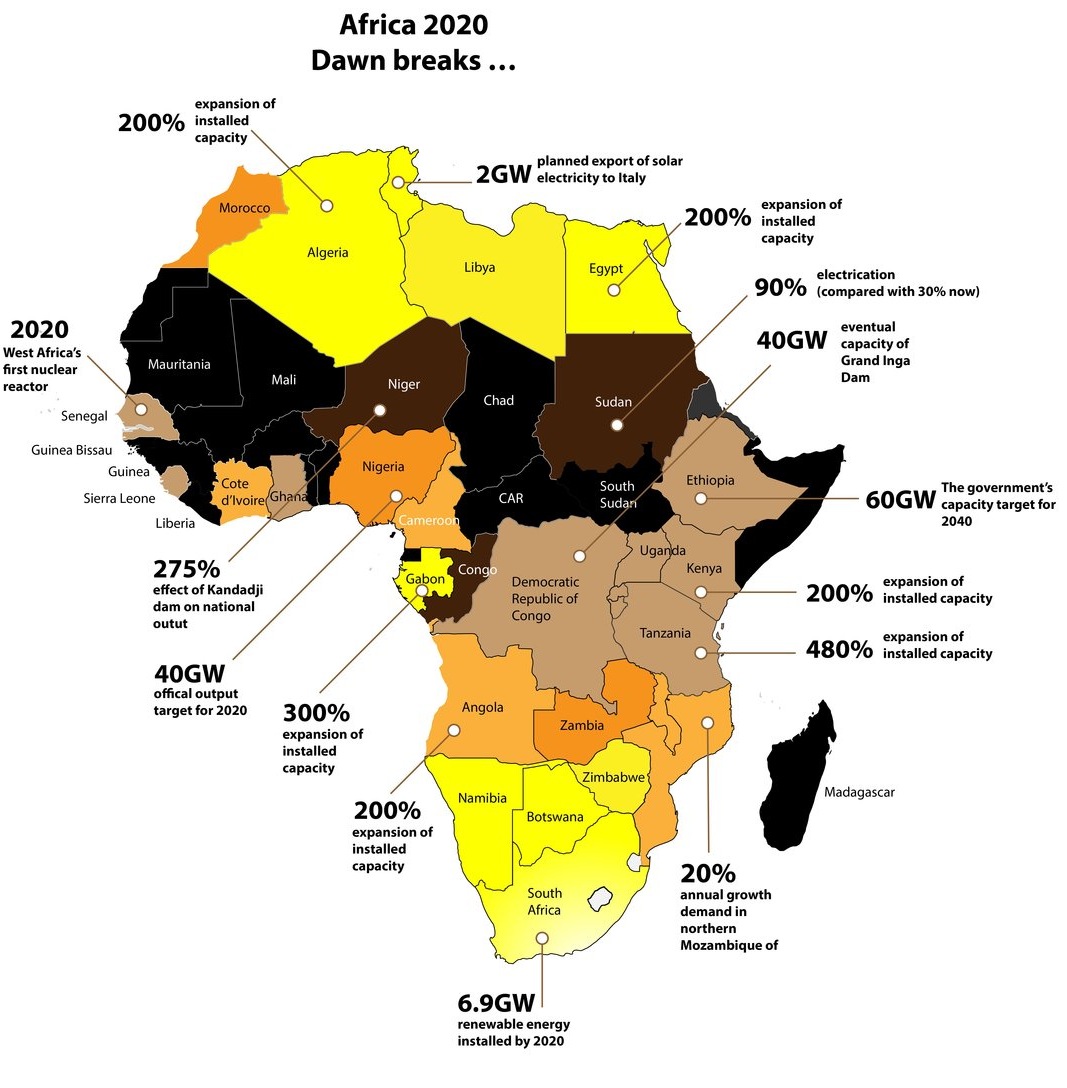

These maps present an assessment of how Africa’s electricity generating industry will develop in the next six years. They are predominantly based on schemes that are either under way, or have received funding, although in some cases, such as Nigeria and Cameroon, we have taken an optimistic view of the government’s stated target.

A map of Africa in 2013, the so-called “Dark Continent” with international comparisons, and a map of how Africa’s electricity generating industry will develop in the next six years

Algeria Capacity is set to triple by 2017 thanks to six gas-powered stations, five built by Korean firms Samsung, Hyundai, GS-Daelim and Daewoo, one by Spanish engineer Duro Felguera.Â

Angola This country will invest $23bn by 2017 to increase its electricity network. The government plans to increase output to 9GW by 2025 compared with 1.8GW now. About 15 plants are on the drawing board, and firms such as Brazil’s Odebrecht are in line to build them. Much additional work will be taken up with repairing the damage left by the 30-year civil war (installed capacity is 1.2GW, but available capacity is 930MW). The biggest single scheme is the Laúca Dam, in northern Kwanza Norte Province, which is designed to provide 5GW of capacity by 2017.

Botswana This industry is coal and oil-based. The plan is to expand the Morupule facility and build a greenfield coal plant to expand capacity from 420MW to 1GW.Â

Cameroon The country aims to increase its generating capacity from 1.1GW to 3GW by 2020.Â

Côte d’Ivoire The government has announced that it plans to increase capacity from 1.2GW to 3.5GW by 2016. The main means of achieving this is private sector investment: 66 projects have been thrown open to independent power producers, among them Ciprel subsidiaryof French construction conglomerate Bouygues. At present generation is split 60:40 between thermal and hydro, and both are to be expanded. The largest project under way is the 275MW hydroelectric plant at Soubre which is being built by Sinohydro.Â

Chad According to Chad’s National Development Plan, 97.4% of households light their houses with oil lamps. Planned developments are modest: rural mini-solar plants to bring electricity to about 33 towns and villages, repairs to the existing, derelict grid, and supplying the city of Bongor from Yagoua in Cameroon.

Democratic Republic of the Congo (DRC) The DRC has an electrification rate of 6%, and a long history of civil war and predatory government has placed 71% of its population below the poverty line. It is also the site of the most ambitious hydroelectric project the world has ever seen: the Grand Inga Dam on the Congo River. Funding is to be provided by the World Bank, the African Development Bank and private investors yet to be found.

The dam would be surrounded by six power stations producing a total of 40GW of energy – an astonishing 17.5GW more than China’s Three Gorges, the biggest dam presently in operation. The first phase, Inga 3, is due to come on line by 2020, producing 4.8GW of electricity. This will quadruple power availability and provide one pre-condition for a change in the fortunes of much of the African continent.

Gabon Hydroelectric facilities generating 166MW provide about 55% of Gabon’s present demand. The government plans to increase production to 1.2GW by 2020. The ambition is to achieve universal access, with excess power exported to neighbouring countries. Plans include hydro, gas and a heavy fuel power station. The largest single project is a 160MW hydroelectric facility being built in Haut Ogooue province by China’s Sinohydro at a cost of $375m.

Egypt The government plans to tackle chronic shortages and a 6% annual rise in demand by cutting subsidies and installing 30GW of additional capacity between now and 2020. Most of the extra capacity will come from plants fired by Egypt’s own gas. Wind and solar will play a supplemental role. Notable schemes include the 1.9GW Helwan South supercritical steam plant being delivered by Japan’s Mitsubishi Heavy Industries and Toyota Tsusho Corporation. Â

Ethiopia The government has impressed many – and angered others – with bold plans to be the powerhouse of Africa. The ultimate aim is to generate 60GW by 2040, but in the shorter term major schemes include the $5bn Grand Renaissance Dam on a tributary of the Nile. It will generate 6GW upon its planned completion in 2017, but Egypt, which sees the dam as an existential threat, has vowed to stop it. Other eyecatching schemes include the 1GW Corbetti geothermal, to be completed in phases to 2021. Wind is slated to generate 800MW and three 100MW solar plants are being built by US companies.Â

Ghana The government has plans to double Ghana’s generating capacity to 5GW by 2016. Among the schemes in progress is the $400m, 155MW Nzema solar plant, the largest in Africa. This is being developed by UK company Blue Energy. There is also a lively debate in the country about whether to build a nuclear plant.Â

Kenya An installed capacity of 1.6GW is set to double by 2020. Hydro power has been hit by drought, so an investment of $1.2bn is planned in solar energy, as part of a grand plan to generate half of the country’s power from photovoltaics by 2016. The Lake Turkana wind plant, the largest in Africa, will generate 300MW and another 200MW is being commissioned. Geothermal is important, with 212MW already installed and another 560MW planned for the Olkaria complex. In the longer term the country plans to build a nuclear reactor. Â

Libya Libya faces an uncertain future. Generating capacity has fallen 5% in the past year and there is little hope for future projects until a political settlement is agreed between the country’s warring militias.Â

Malawi According to the UN, demand from the mining industry is going to boost demand from 740MW to 1.4GW by 2020. This will be met with new coal-fired plants, which Chinese and Indian firms have been vying to build over the past two years.Â

Mauritania This Saharan country has a total generating capacity of 263MW. Development plans concentrate on providing energy for cooking. Â

Morocco The visionary Desertec plan, backed by German engineer Siemens, to create a 100GW solar industry in Morocco, able to supply 20% of Europe’s total demand, was abandoned last year. The plan on the table now is the Moroccan Energy Strategy, which aims to reduce the kingdom’s electricity imports – at present these account for 25% of the total imports of Morocco. Another 1.7GW of generating capacity is planned for 2020.

Mozambique A generating capacity of 2.4GW comes entirely from the Cahora Bassa dam but almost all that power is exported to South Africa. However, a natural gas discovery has led to the commissioning of nine thermal plants with a total capacity of 800MW and a $1.8bn transmission line to act as the spine of a fledgling national grid. Together with new hydro, 5GW of extra capacity will come online by 2020.Â

Namibia This country has a population of only 2.3 million. About 60% of the country’s electricity is imported from South Africa. Small scale renewable schemes are in train, but by far the biggest project is the 800MW Kudu gas scheme, much delayed, but scheduled for completion around the end of 2017. This will triple installed capacity.Â

Niger Niger is set to be transformed by the Kandadji dam, which will increase to country’s installed generating capacity from 134MW to 370MW.Â

Nigeria The government is targeting a massive expansion of generating capacity, from 5.9GW to 40GW. There is some scepticism about this figure, however, and observers have suggested that, given Nigeria’s record of public maladministration, it is unlikely to get much beyond 8GW. One indicator of Nigeria’s eventual success is the progress of the 3GW Mambilla Dam, a scheme first proposed in 1982. After murky negotiations with a number of Chinese firms and a meeting between presidents Goodluck Jonathan and Xi Jinping in May, a consortium led by Sinohydro is to carry it out. According to the Nigerian press, work on site is to begin in October.

Senegal The country’s generating capacity of 638MW comes mostly from the Cap des Biches thermal plant. Germany has been helping the country to develop its renewable energy and there are plans for a nuclear reactor, however the main development will be Africa Energy’s 300MW coal-fired plant, which is due to be complete by 2017.Â

Sierra Leone The 50MW Bumbuna dam is the principal source of the country’s 145MW of generating capacity. Work is underway to expand that to 250MW, and it has just been announced that $100m is to be spent on a thermal plant. Â

South Africa More than 90% of South Africa’s 44GW comes from coal. By 2020, that is going to be joined by 9.6GW of nuclear energy as part of a $29bn nuclear programme. It is also building the Medupi and Kusile coal plants, each of which can generate 4.8GW. This coal and uranium strategy will be supplemented by solar and wind power: about $5.5bn has been invested in its Renewable Energy Independent Power Producer Programme, and it is aiming to install 6.9GW by 2020. A recent Ernst & Young report suggested it would have 8.4GW of solar alone by 2030.Â

Sudan Sudan generates 3.7GW from hydro. Recent capacity increases have been delivered with help from China International Water & Electric Corporation, and funding from Kuwait and Saudi Arabia. The country plans to extend electrification from 30% to 90% of the country by 2020.

Tanzania A huge find of natural gas and an influx of Chinese capital and engineering expertise is beginning to transform this country. The initial aim of the state utility Tanesco is to create a national grid and increase per capita electricity use to 81kWh to 200kWh by 2016. By 2020, the government’s Power System Master Plan calls for installed capacity to rise from 840MW to 4GW, almost a fivefold increase.

Tunisia The Tunisian solar plan includes 40 projects that are intended to reduce the country’s reliance on gas, which now makes up 90% of its energy mix. The biggest scheme is Nur Energie’s 2GW concentrating solar plants.Â

Uganda The government hopes to expand the country’s installed capacity from 540MW at present to 1.2GW by 2020. The solution envisaged is large-scale hydropower, with the Ayago (500MW), Kalagala (600MW) and Murchison Falls (450MW) sites earmarked for exploitation.Â

Zambia Zesco, the state electricity utility, plans to double its electricity generation capacity to 2.8GW in the next five years, mainly using coal-fired plants. Although Zambia is essentially without grid electricity (only 3% of the country is electrified) much of that new power will go to its energy-intensive copper industry (the Konkola mines alone require a load of 250MW to operate). A budget of $5.3bn has been set aside for this.

Zimbabwe China is planning to build a nuclear plant in this country by 2020 in exchange for the right to mine uranium. At present the 920MW Hwange coal-fired station supplies almost half the country’s power. This is due to be supplemented by three hydro schemes, the 300MW ZPC solar plant and a huge coal station, the 1.2GW Western Area scheme. Not counting the nuclear facility, generating capacity is set to rise by 4.1GW.

Comments

Comments are closed.

However highly laudable all of this may seem, it is highly necessary for each and every country so engaged to urgently and adequately educate and train sufficient numbers of each and every power sector specialist engineers ,technicians and trade operatives to optimally run and maintain such very costly power generation installations!