The value of projects awarded in the normally bullish Gulf Cooperation Council (GCC) area fell significantly in the first six months of this year, a study has shown.

Countries in the region, most of which rely on exporting oil and gas, have seen national budgets hit by the low price of oil, while a diplomatic stand-off between Qatar and a group allied to Saudi Arabia has also increased tension.

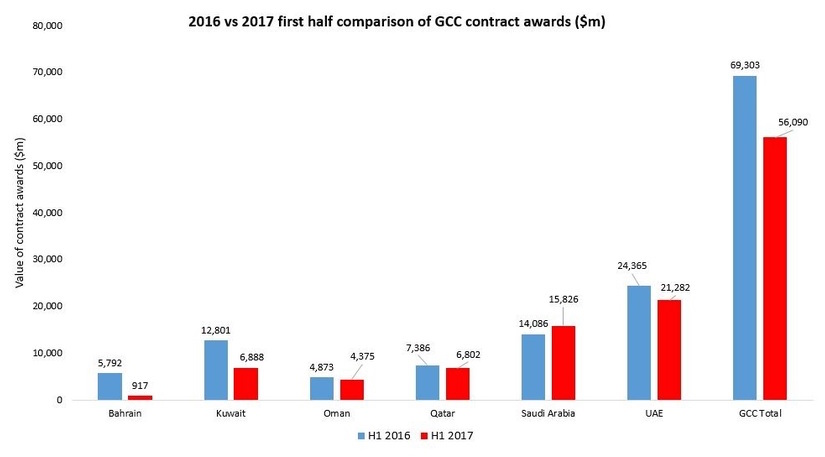

According to the latest data from MEED Projects, a project tracking service, just $56bn worth of contracts were awarded in the first six months of 2017 compared with $69bn worth of deals over the same period in 2016, a 19% fall.

With the exception of Saudi Arabia, every country in the region experienced lower contract award values year-on-year, with the most marked falls seen in Kuwait (46%) and Bahrain (84%).

2016 vs 2017 first half comparison of GCC contract awards ($m) (MEEDProjects.com)

Even Dubai, which has hitherto been the most robust and active of the GCC projects markets, experienced a slight dip between the two periods.

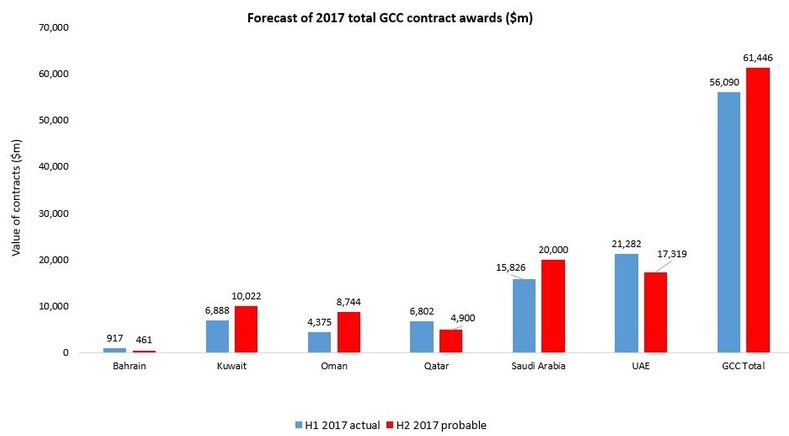

The prognosis for the second half of 2017 is brighter, however. Based on its tracker’s pipeline of projects under bidding, plus contracts already awarded in July and August, MEED Projects forecasts a total of $61bn to be let in the second half of this year.

If that figure is reached, the total for 2017 would be $117bn, roughly equivalent to value of contracts awarded in 2016.

On a country level, the UAE, led by the Dubai real estate and transport sectors, remains the largest single market with about $38bn worth of contract awards. It is followed by Saudi Arabia at close to $36bn, and then Kuwait at $16.8bn.

“Although market performance year to date has been sluggish, there have been signs of a pick-up in activity,” said Ed James, Director of Content & Analysis at MEED Projects.

“The award of more than $5bn worth of EPC contracts on the new Duqm refinery in Oman at the beginning of August, plus a raft of new project announcements in Dubai, and the gradual re-emergence of activity in Saudi Arabia have provided a degree of impetus that points to a strengthening market.

Forecast of 2017 total GCC contract awards ($m) (MEEDProjects.com)

“There’s no doubt that the past two years have been tough for the projects supply chain as government spending has slowed,” adds James. “But with construction companies now more efficient, the private sector more active and the number of PPP projects growing by the week, there is cause for optimism.

“Longer term, there is even more reason to be hopeful. Currently, there are over $2 trillion of known active projects in the pipeline across the GCC according to MEED Projects data. The majority of these are infrastructure schemes that are essential to the future prosperity of the region, job creation and economic diversification. While inevitably not all will come to fruition, we can be confident that there is still a large amount of work to come regardless of the oil price.”

Top image: Dubai in its construction heyday, 2008, with Dubai Marina in background and Mina Jebel Ali in foreground (Basil D Soufi/Wikimedia Commons)

Comments

Comments are closed.

Good to know the future prospects seems brighter. It would be nice to have a graph showing split of infra, buildings and O&G projects.